The triple pressures of supply-demand imbalance, high costs, and tight production capacity have all affected the entire value chain, from the upstream wafer factories to the downstream end manufacturers.

1. Storage Chips: The "Super Cycle" Driven by AI

Interior view of an AI server data center, showcasing high-performance computing chips and high-speed storage modules, highlighting the urgent need for storage in computing scenarios

1.1 Price Surge Reaches Record High

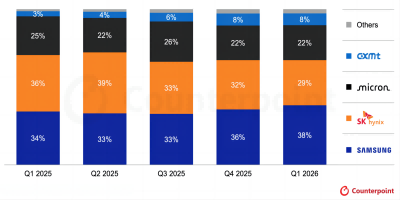

Since 2025, the global storage chip market has completely left the low-price cycle and entered a strong rebound led by AI demand. The prices of the two core categories, DRAM and NAND Flash, have soared all the way, becoming the core protagonists of this price increase wave.

Market data shows that high-frequency and high-capacity models for servers and high-end laptops have seen a price increase of directly exceeding 30%; in the terminal market, it is more obvious: notebook memory prices have doubled in half a year, the price of solid-state drives has doubled, the price of 1TB SSD has dropped below 1,000 yuan, the 2TB version has firmly stood at over 200 yuan, even the high-speed TF cards for cameras, the 128GB specification has also risen to over 200 yuan, and different brands only have a small price difference.

1.2 Supply-Demand Imbalance Is the Core Driver

This round of storage price increase is essentially a two-way imbalance between the supply side tightening and the demand side explosion. It is difficult to be quickly alleviated in the short term:

✅ Supply Side: Insufficient production capacity, slow expansion

The advanced process production capacity of global leading wafer factories is saturated, and the production capacity of high-end storage chips is in short supply. The release cycle of new production capacity may take one and a half to two years.

The manufacturing process of storage chips is complex, and the difficulty of yield control is high. It is impossible to quickly make up for the gap through rapid expansion.

The cost of raw materials such as silicon wafers and photoresist continues to rise, further pushing up production costs.

✅ Demand Side: AI Computing Power, Sparking Essential Demand

The demand for AI servers has grown explosively, becoming the largest growth market for storage chips. The storage capacity requirement per server has increased exponentially.

The construction of 5G/6G equipment, intelligent driving, data centers, and energy storage systems is accelerating, continuously diverting storage production capacity.

The upgrade and replacement of consumer electronics and digital devices have led to a steady increase in the demand for large-capacity and high-speed storage.

II. Resistors and Capacitors: The "Price Increase Storm" of Passive Components

Close-up of the automated production line for resistors and capacitors, showcasing the precise manufacturing process and the component inspection procedures, highlighting the manufacturing threshold of passive components

2.1 Collective price hikes for passive components, exceeding expectations

Entering 2026, the price increase trend in the passive components industry continued to intensify. Leading domestic and foreign manufacturers such as Kintetsu, Huaxinke, Panasonic, Fenghua Hi-Tech, and Songluo Electronics successively released official price adjustment notices, with the prices of all categories rising:

MLCC (Multilayer Ceramic Capacitors): The full range saw an increase of 10% - 15%, with the automotive-grade and industrial-grade models experiencing even higher increases

Surface-mount resistors: General models saw an increase of around 10%, while special specifications and high-precision models saw an increase of up to 20%

Tantalum capacitors: Panasonic and other international manufacturers had the largest price adjustment, with some models experiencing an increase of over 30%

2.2 High costs drive up prices in the industry

Passive components may seem insignificant, but they are the "basic components" of electronic devices. The core reason for this round of price hikes lies in the double increase in raw material and manufacturing costs:

The cost of raw materials has skyrocketed

The price of precious metals has gone out of control: The price of silver has soared by 201% year-on-year, becoming the biggest cost pressure for passive components

The prices of basic metals have risen: The prices of industrial metals such as copper, tin, and nickel have continued to increase, directly pushing up the cost of component substrates

Supplementary materials are in short supply: The supply and demand of key materials such as glass fiber cloth and ceramic powder are tight, and their prices have also risen simultaneously

2.3 Manufacturing costs continue to rise

The costs of industrial electricity, natural gas and other energy sources have increased, putting more pressure on production line operations

The labor costs and research and development expenses in the manufacturing industry have steadily risen

Global logistics transportation costs and customs clearance and warehousing costs have significantly increased

III. In-depth Analysis of the Impact on the Industrial Chain

The increase in the prices of electronic components is not a fluctuation in a single link, but spreads along the entire chain from "upstream" to "midstream" to "downstream", and enterprises at different links present a starkly contrasting situation.

3.1 Upstream Enterprises: Direct beneficiaries, significant profit increase

Wafer foundries: Capacity utilization rate remains high, orders are fully booked, bargaining power has significantly improved

Material suppliers: Sufficient orders for silicon wafers, precious metals, and chemical materials, profitability has continued to recover

Equipment manufacturers: Benefiting from the industry's expansionary demand, sales of semiconductor production and testing equipment have increased

3.2 Midstream Enterprises: Pressure Transmission, Difficult Balance

Semiconductor manufacturers: Say goodbye to low-price competition, significant profit recovery, but still need to balance supply capacity and demand

Passive component manufacturers: Urgent need to transfer cost pressure to the downstream, and the adjustment pace needs to take into account both the market and customers

Electronic distributors: Difficulty in inventory management increases, and the risk of stockpiling rises under price fluctuations

3.3 Downstream End Users: Cost Pressures, Profit Compression

AI Server Manufacturers: Experiencing the greatest cost pressure, with a high proportion of storage components, and the overall unit cost has significantly increased.

Smartphone/Laptop Manufacturers: BOM costs have risen, pricing space is limited, and profits have been squeezed.

Automotive Electronics Manufacturers: Supply of automotive-grade components is tight, with both shortage and price hikes causing double problems.

Consumer Electronics Manufacturers: The profit margins of low-end products have further shrunk, and industry consolidation is accelerating.

IV. Future Trend Outlook

4.1 Short-term Trend: Price Increase Will Continue

In the short term, the price increase trend of electronic components is unlikely to reverse. The core logic remains unchanged:

The demand for AI computing power continues to surge, and the shortages of high-end storage and automotive-grade passive components are difficult to fill.

The construction period of advanced production capacity is long, and the supply-demand gap will not be alleviated within 1-2 years.

The cost pressure of precious metals and basic metals still exists, and the cost end supports the price to remain at a high level.

4.2 Long-term Impact: Industry Structure Transformation

Accelerated Technological Iteration: Components with higher performance, smaller size, and lower power consumption have become the mainstream, and the trend of high-endization is evident

Rapid Domestic Substitution: Enhanced awareness of supply chain security has given domestic high-quality component manufacturers an opportunity to break through

Increased Head-Effect: Leading enterprises with technological, scale, and production capacity advantages have further expanded their market share

V. Suggestions for Response Strategies

In the face of this AI-driven price increase cycle, different entities need to make targeted arrangements to reduce risks and seize opportunities.

5.1 For manufacturers: Stabilize supply chains, optimize product structure

Optimize inventory management, establish a safety stock mechanism to avoid risks from short-term price fluctuations

Strengthen cooperation with core suppliers, sign long-term supply agreements, and secure stable sources of supply

Accelerate product structure upgrading, shift towards high value-added and high-tech barrier products to offset cost pressures

5.2 For Purchasers: Multiple Channels, Strict Cost Control

Diversify procurement channels to avoid reliance on a single supplier and reduce the risk of supply disruptions

Lock in purchase prices in advance and sign long-term pricing agreements with suppliers to mitigate the impact of price increases

Optimize product design and select cost-effective components to control costs at the source

5.3 For Investors: Make Rational Investments, Focus on Leading Companies

Pay attention to industry leaders with advanced technology and significant scale effects, as they have stronger resilience to cycles

Take advantage of the domestic substitution trend and focus on domestic component enterprises with core technologies

Rationally view cycle fluctuations. The electronics industry has strong cyclical characteristics, so avoid blindly chasing high prices

Summary:

This round of electronic component price hikes is not only an inevitable outcome of the explosive demand for computing power in the AI era, but also an important opportunity for the reconfiguration of the industrial chain. The short-term cost pressure is a challenge, while the medium- and long-term technological upgrades and domestic substitution represent a rare opportunity.

*Disclaimer: The article is sourced from the internet. In case of any dispute, please contact customer service.