In 2026, the global electronics industry witnessed an unprecedented chip price increase wave. This wave spread from the high-end computing power sector to consumer electronic terminals, affecting every link of the entire industry chain. Whether it was cloud computing infrastructure deployment, enterprise production and manufacturing, or ordinary consumers' daily digital purchases, all were impacted to varying degrees. In this major market upheaval, how to accurately grasp market trends, avoid cost risks, and secure a stable supply chain became the core issue for all relevant practitioners and enterprises.

From the perspective of the computing power market, the price increase of chips has become an undeniable fact and has become the core variable influencing the industry landscape. As a global giant in the chip sector, NVIDIA's rental prices for its high-end chips have been soaring, serving as a leading indicator for the price increase in the computing power market. Among them, the rental price of the H200 model chip has risen to 7.5-8.0 yuan per hour, with an increase of 25%-30% compared to before. Even with the significant price increase, the market demand remains in short supply, and its orders have been queued up until 2027. Due to factors such as supply chain tensions in the domestic market, there is even a 20% premium. Many enterprises, in order to meet the demand for computing power, have no choice but to accept the reality of purchasing at a high price.

Domestic cloud service providers have also followed suit. The computing cards such as Pingtouge Zhenwu 810E under Alibaba Cloud have adapted to the market trend and their prices have increased by 5% to 34%. The prices of their related intelligent computing and storage products have even risen by as much as 30%. Following closely behind, major domestic cloud service providers like Baidu Intelligent Cloud and Tencent Cloud have successively issued price adjustment notices. The prices of AI-related computing and storage services have generally increased, directly causing a significant rise in related costs for enterprises, especially small and medium-sized enterprises, which are facing a huge pressure of a sharp increase in computing costs. Many enterprises have had to reduce their investment in computing resources, affecting the pace of business development.

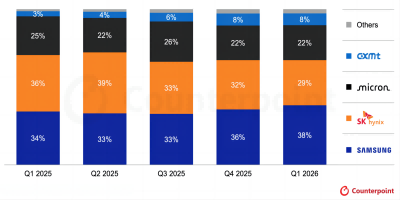

The prices of storage chips have also soared simultaneously, further squeezing the profit margins of mobile phone manufacturers. LPDDR5X memory and UFS 4.2 flash memory, as the core storage components of mobile phones, saw their purchase prices increase by 8% to 12% year-on-year. Meanwhile, due to the shift of advanced production capacity by storage giants such as Samsung to high-bandwidth memory (HBM), the supply of consumer-grade storage chips has been further constrained, leading to the continuous rise in storage chip prices. The prices of some models of memory have even increased by more than 30% compared to the end of 2025. The proportion of storage chips in the overall cost of mobile phone devices has soared from the original 10%-15% to 30%-40%. In mid-range phones, this proportion is even approaching 50%.

The significant increase in costs has been directly passed on to the final products. For mobile phone brands that emphasize cost performance, such as Redmi, the cost of their flagship models has risen by 300-500 yuan. Many models have had to raise their prices. In the second quarter of 2026, the entire mobile phone industry witnessed a wave of price hikes. Flagship models generally saw a price increase of 300-1000 yuan, mid-range models saw a price increase of 100-300 yuan. Consumers need to spend more money when purchasing mobile phones. Many essential consumers were forced to postpone their upgrade plans. For mobile phone manufacturers, their profit margins have been significantly reduced. They are facing a difficult choice between losing market competitiveness due to price hikes and incurring losses if they do not raise prices. The industry shakeout has further intensified, and the survival pressure on small and medium-sized mobile phone manufacturers has become increasingly huge.

This overall price increase for chips is not an isolated event; it is the result of multiple factors working together. It reflects the deep-seated contradictions in the global electronic industry supply chain. On one hand, the acceleration of global digital transformation, the widespread use of various intelligent devices, data centers, and applications related to artificial intelligence, has led to an explosive growth in chip demand. Especially, the demand gap for high-end chips continues to widen, and chip manufacturers' production capacity cannot meet the market demand in a timely manner. On the other hand, the production cycle of advanced process chips is long and the technical difficulty is high. The production capacity of major global wafer foundries such as TSMC and Samsung is growing slowly and cannot keep up with the growth rate of market demand. Especially for advanced processes like 3nm and 4nm, the production capacity is always at full capacity, further exacerbating the shortage of chip supply.

For consumer electronics companies, the profit margin is continuously shrinking, and they are faced with the difficult choice of either raising prices or reducing configurations. The industry shake-up will further intensify. Under such circumstances, for companies to survive and develop, they must optimize supply chain management and reduce procurement costs.

For the entire electronics industry, this wave of chip price hikes is both a challenge and an opportunity to promote the development of domestic chip and component industries.

*Disclaimer: The content is from the internet. In case of any dispute, please contact customer service.